Latest developments

Australia’s resource and energy export earnings are forecast to reach a new record of $459 billion in 2022–23.

- Energy prices have fallen from record highs, on easing fears of Northern Hemisphere winter shortages, but will likely stay above pre-war levels in 2023, as some Russian energy supply becomes stranded.

- High energy prices and strength in the US dollar are driving a surge in export earnings. After a record $422 billion in 2021–22, resource and energy export earnings are forecast to lift to $459 billion in 2022–23, before falling back to $391 billion in 2023–24.

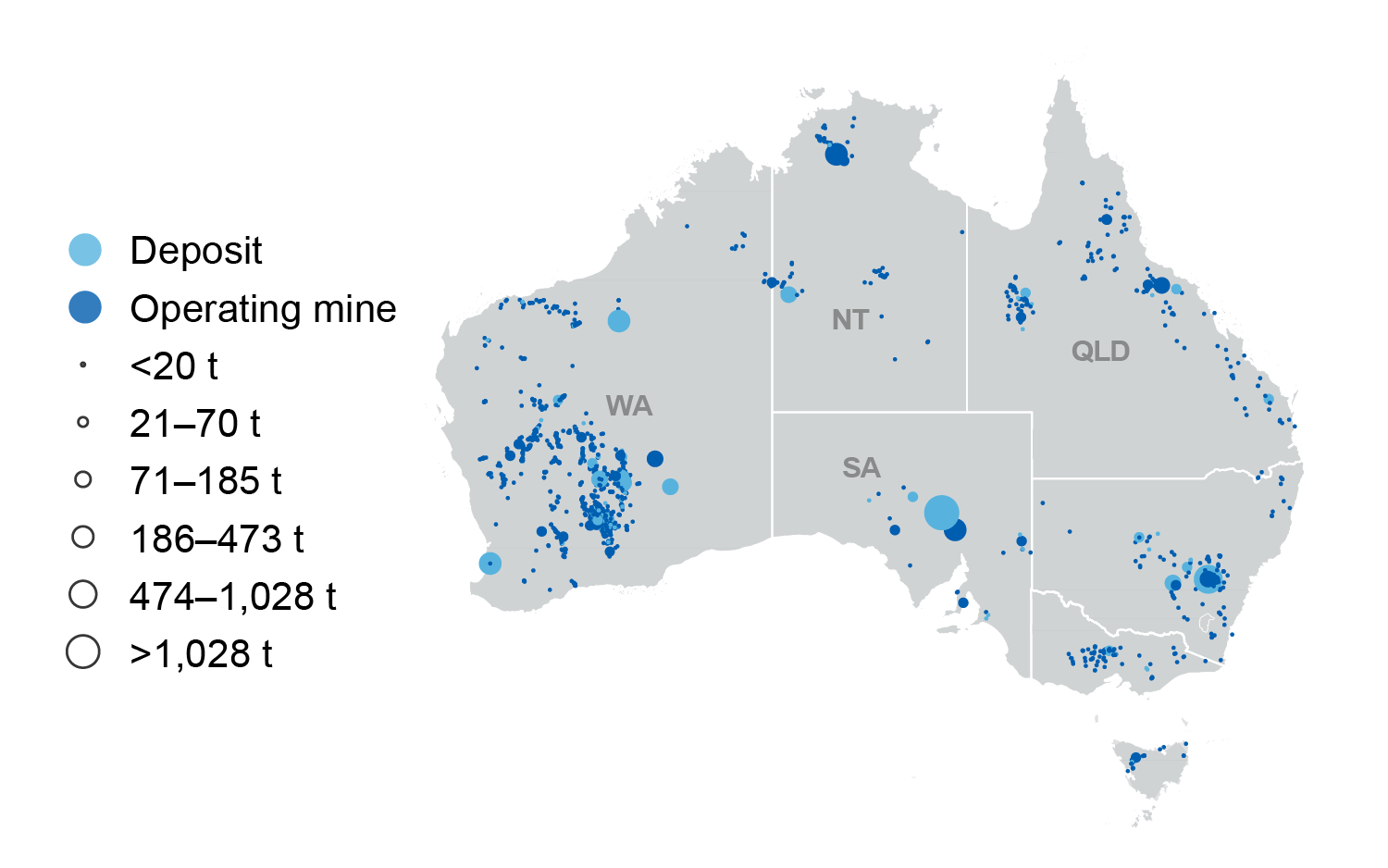

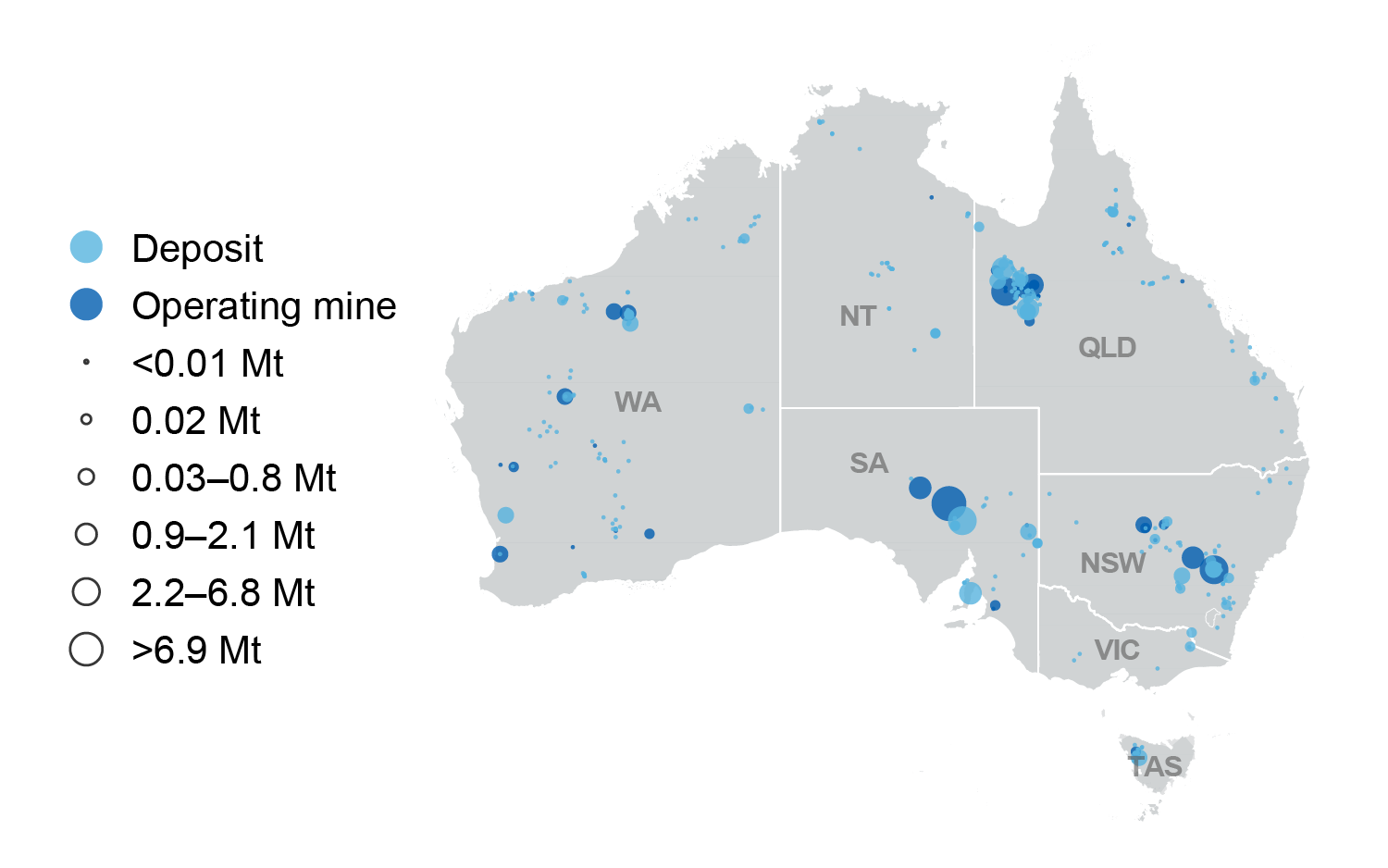

- Lithium exports are set to earn $16 billion in 2022–23, becoming our sixth-largest resource and energy export.