Latest developments

Australia resources and energy exports are passing a peak.

- In net terms, the outlook for Australian resource and energy commodity exports has improved slightly since the September edition of the REQ. The world economy has not slowed as sharply as feared a few months ago and the Chinese Government has taken further measures to stabilise the nation’s residential property sector, maintaining demand for a range of resource commodities.

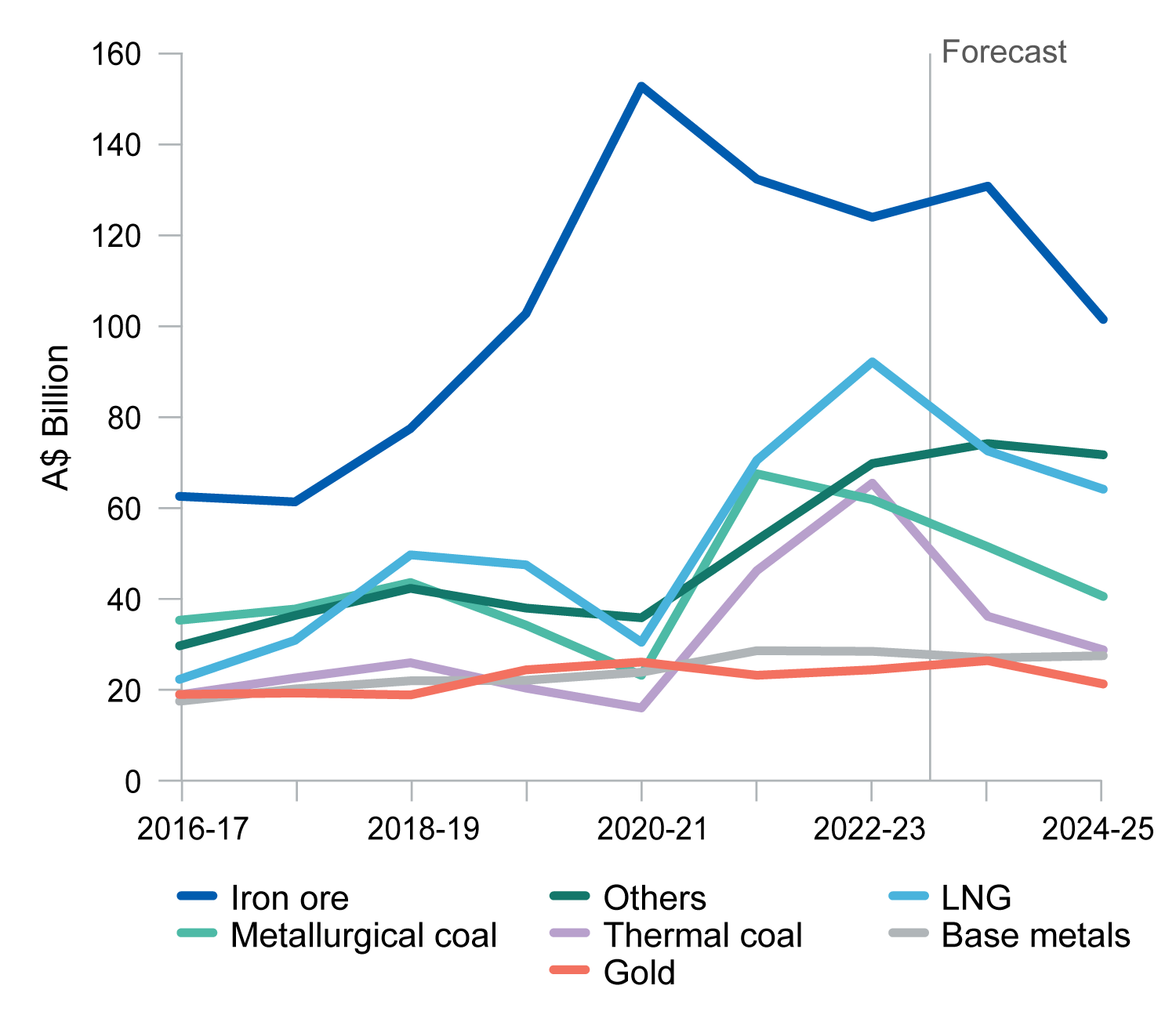

- The latest forecast is for weaker growth in world demand and improving world commodity supply to reduce Australia’s resource and energy export earnings from a record $466 billion in 2022–23 to $408 billion in 2023–24. A further decline seems likely in 2024–25, as commodity prices soften further and monetary policy expectations imply a stronger Australian dollar.

- Key September quarter price developments include:

- higher iron ore prices as Chinese demand continues

- higher uranium prices as countries re-evaluate nuclear power

- lower lithium prices due to high stockpiles and concerns around near term EV demand.